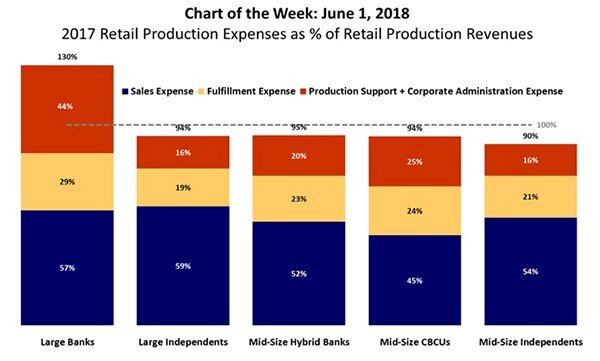

In 2017, mid-size independent mortgage lenders performed much better than their peers in terms of managing expenses of their retail production. However, even with better performance, data shows that their loan production expense was almost equal to the revenues they were earning. Similarly, large banks struggled to control all costs, particularly production support and corporate overhead expenses, which were the highest at 44 percent of revenues (compared to 16% for mid-sized independent lenders). Large banks’ overall production expenses were higher than their production revenues – meaning they were losing money on every loan.

So what contributed to the expenses? Across all peer groups - except mid-size community banks and credit unions - more than half of revenues went to cover sales expenses alone. Although sales are the largest chunk of the cost of loan production, fulfillment expenses also ate up a substantial part of the revenues. So let’s look a little deeper into this. As can be seen from the accompanying graphic (Source: MBA Chart of the Week: 2017 Retail Production Expenses), fulfillment expenses range from a low of 19% to a high of 29% of revenues. Among the various types of lenders, large banks have the highest fulfillment expenses (as a percent of revenues). This is clearly a disadvantage for larger banks, and they must look deeper into their origination processes and identify areas that can reduce expenses – typically identified by looking at wastage of time, and wasted human efforts.

What are the potential reasons for higher fulfillment costs?

Our experience with mortgage processes and lenders in the U.S. over the last decade or so indicates that some of the areas that typically involve wasted time and effort (and therefore increase costs) and are easier to address include:

- Longer cycle time from application to processing

- The lag time in communication with borrowers

- Multiple file touches by processor and underwriters

- Inaccurate quality checks leading to rework and higher compliance penalties.

There could be several other reasons, but these are the ones which we have identified that are easy to identify and fix as well.

What are potential solutions that lenders can easily adapt to keep fulfillment costs down?

1. Use technology for borrower document collection in application processingEvery time a customer goes through a loan application process, the borrower is asked to submit a number of documents that decide their eligibility. These documents are collected and checked by a processor and then the document file is moved to an underwriter for a Conditional Loan Approval (or CLA).

Although this seems pretty straightforward and a one-time collection, in reality, this requires multiple rounds between the borrower and the processor to get all the appropriate documents in place, increasing the time to move forward, as well as reducing the efficiency of processing. Moreover, the processor may end up focusing on trying to wrap-up a particular loan in hand, in-turn de-prioritizing other new ones coming in, and leading to further backlog. Obviously, these add to the overall cost of the entire process of taking a loan application to final closure. The question is, can borrowers and processors be empowered with a process supported by technology that reduces the back-and-forth and potentially automates the process? The obvious method is to use cutting-edge technology (ICR/OCR, RPA, AI, Mobile App, etc.), but that means a fair amount of investment dollars, as well as process change and learning for processors, LO’s and even the borrowers. Alternatively, a simpler low-cost, quickly implementable approach is the use of ‘algorithms’.

An algorithmic checklist that not only identifies the missing documents but also informs and follows-up with processors, LO's to ensure they have the right documents before submission to underwriting can really help streamline the entire process. We have been able to implement this for Banks and achieved reduction of 60% in Loan app to Underwriting times. Although this may sound like a low-tech solution, it actually converts a deep understanding of the real-world process of document collection and verification, with easily implementable technologies, to reduce the time to get a file to an underwriter to as low as 24 hours.

An algorithm-based checklist that checks the collected documents and makes sure underwriting requirement are as per compliance, can be a savior for banks that need to keep their technology costs low, but who still want to implement quick solutions based on technology.

2. Ensure processors submit CLA ready file for underwriting, really quickly

We all agree that the authority to sanction a Conditional Loan Approval is only with an underwriter. But that does not mean that the relatively more expensive underwriter should do unnecessary groundwork before getting to the approval. Think about the time and cost we would be saving if the processor is able to submit a CLA-ready (or Conditional Loan Approval ready) file to underwriting. As easy as this may sound, the implementation of this process requires a combination of optimum services and technology backed by knowledge of the nuances of exactly what is needed to reduce the file ‘touches’ by an underwriter. Every touch point since the application has to be streamlined to a high degree. Usage of technology, historical data for trend analysis, algorithms, communication modules, and more will come into play to make sure that the processor is able to submit a CLA ready file for underwriting.

There are domain experts who have made this possible and lenders who have benefitted with cost reduction and faster closings. In our case, we have helped customers reach a stage of 1-touch underwriting after 3-4 weeks of implementation of these services and technologies.

3. Use QC and QA to deliver more than just complianceAfter 2008, and with the introduction of regulatory reform, lenders have introduced Quality Control and Audit with the main purpose of complying with regulations. That’s because one compliance or quality check that is not carried out correctly can potentially cost millions in fees and fines. Compliance is a need not just for regulators, but the thinking of investors has changed and they also want to make sure they do not end up with portfolios with compliance issues, leading to salability or valuation problems.

As lenders, having all of this investment in place already to ensure compliance, it makes sense to utilize it for something that is becoming critical as the mortgage volumes decline – making processes efficient and reducing costs. A new breed of providers are putting into place methodologies that not only ensures better loan quality and compliance, but uses the information garnered from the QC activities at any and every stage, to build data intelligence which can directly influence sustainable process improvements - not just for the process being checked, but across the whole mortgage lifecycle. This is something we have started actively implementing and delivering on for our customers now – and this is fast making QC and QA not just a cost center, but a contributor to process improvements affecting the bottom-line of the organization positively.

The conclusion:Today, mortgage loans must be done right with great scrutiny throughout the entire production process. That would typically add cost and effort to the process. On the other hand, competitive pressure, demands from borrowers, and tighter margins require lenders to engage customers, be aggressive with timelines while maintaining loan quality and keeping costs low. This is needed to be profitable and to grow. That is where lenders are using the help of experienced providers to integrate technology, optimized processing services, and intelligent process analytics to drive mortgage processes and make it all happen. These optimal services, which require low investment to initiate, are eventually helping to improve the bank’s bottom-line and help leave behind the competition in an increasingly tough mortgage environment.

Contact us at CoforgeBPS@coforge.com or visit https://www.coforge.com/bps/ to know more about these and our other solutions.

Explore Coforge's BPS success stories. Discover how we drive efficiency, innovation, and customer satisfaction across various industries.

Related reads.

About Coforge.

We are a global digital services and solutions provider, who leverage emerging technologies and deep domain expertise to deliver real-world business impact for our clients. A focus on very select industries, a detailed understanding of the underlying processes of those industries, and partnerships with leading platforms provide us with a distinct perspective. We lead with our product engineering approach and leverage Cloud, Data, Integration, and Automation technologies to transform client businesses into intelligent, high-growth enterprises. Our proprietary platforms power critical business processes across our core verticals. We are located in 23 countries with 30 delivery centers across nine countries.