By Satya Syam Puppala

Background

In Banking, the default risk on a debt that arises from a borrower who fails to make the required payments is called Credit Risk. Any lender would include this as a first resort which includes principal and interest along with disruption to cash flows and the collection cost. The loss may be partial or even complete

Difference between Traditional and Current Methodologies

Calculating the Credit Risk is not new in Banking. Traditional Models in Credit Risk is calculated mainly on five C’s 1) Credit History 2) capacity to repay 3) capital 4) the loans condition, and 5) associated collateral. Some companies have a dedicated department only for assessing the credit risk of its current and potential consumers.

It is true that higher borrowing costs are always associated with higher credit risk levels but may not be correct in all the cases

Modern models in CreditRisk can be evaluated with many factors that may contribute to improve the more accuracy in developing Risk Models. These factors contribute to find out the borrower’s ability to repay the loan. To assess the credit risk the lenders shall also consider CustomerID, CheckingStatus, LoanDuration, CreditHistory, LoanPurpose, LoanAmount, ExistingSavings, EmploymentDuration, InstallmentPercent, Sex, OthersOnLoan, CurrentResidenceDuration, OwnsProperty, Age, InstallmentPlans, Housing, ExistingCreditsCount, Job, Dependents, Telephone, ForeignWorker and Risk are few of the attributes that needs to be considered. Considering the current computational & processing power of computers, any number of attributes with any data size can be handled efficiently without negotiating the performance.

How Machine Learning and Data Science can help in building effective Credit Risk Models

Technologies associated with Data Management, Big Data, and Artificial Intelligence helps to build sophiscated real time Credit Risk models. Using Data Science, Machine Learning and Deep Learning analysis, banks are now able to carry out a complex task like credit risk predictions, monitoring, model reliability, and predicting loan default probability.

Machine learning algorithms enhance predictive abilities and can, therefore, help the lenders receive real-time insights about their current and potential borrowers. This shall allow them to disburse loans to the right set of customers.

Value proposition Coforge brings to its Customers

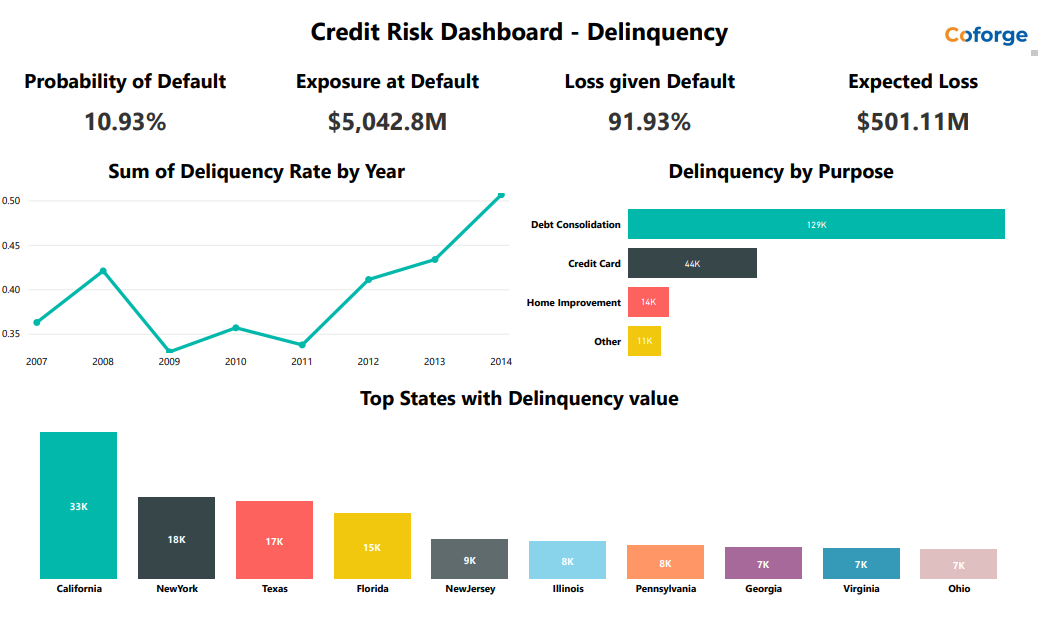

Apart predicting credit risk for Debtor, calculating overall Expected Loss to the financial institution, projecting those results into Visualizations is key to any credit risk analyst to take quick decisions based on data.

Calculating Expected Loss for Bank or Institution

After the recession in 2008 Banks started calculating over all Expected Loss by using PD, EAD and LGD.

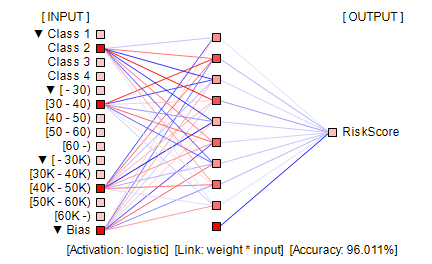

PD stands for Probability of Default; it is assigned to each risk measure and represents as a percentage the likelihood of default. PD can be calculated from historical data of past-due loans.The PD score is generated by using the pattern recognition algorithms such as Naïve Bayes, Ensemble models like Bagging & Boosting, Deep Neural Networks such as CNN

EAD stands for Exposure at default; this is the predicted amount of loss a Bank may be exposed to when a debtor defaults on a loan. This is the value given by Bank’s internal risk management default models to estimate respective EAD systems.

LGD stands for Loss Given Default; this measures the expected loss in percentage. LGD represents the amount unrecovered by the lender after selling the underlying asset if a borrower defaults on a loan. Usually this value is generated from third party lenders.

Expected Loss = EAD x PD x LGD

Data Visualizations Reports for the Calculated and Predicted Risk scores

The human brain processes information, using charts or graphs to visualize large amounts of complex data is easier than poring over spreadsheets

Data visualization is the process of translating data and metrics into charts, graphs and other visuals. The resulting visual representation of data makes it easier to identify and share real-time trends, outliers, and new insights about the information represented in the data. Below visualization shows how easily we can analyze the Credit Risk dashboard at a glance.

Challenges in developing Credit Risk Models

- Continuous changes in Market dynamics, specifically in this pandemic time

- Exponential increase in data related to Customer 360, Market, Commercial and Transactional data

- Data Governance and Management on Tera bytes of Data Warehouses / Data lakes

- Computational challenges in Processing and Mining the data; specifically building models using Neural Networks

- Deployment and Monitoring of AIML models where frequent changes are required to the models

Future of Credit risk modeling

Credit Risk evaluation happens continuously before and after providing the loans to the customers.

There is a probability that even existing customer may go bankrupt over a period and their Risk probability may increase. This can capture by continuous monitoring of Customer data along with Transactional data of customer withdrawals, credit history and with external datasets related to Market dynamics.

With the help of niche technologies in the area of Data Management, ML Frameworks and High Performance Computing(HPC) it is possible to provide Integrated, Secured, Efficient and Reliable Credit Risk Models; where stakeholders get real time notifications, alerts and Insights.

Best Practices in delivering Credit Risk Models

- Reduce time to market for credit risk models through streamlined implementation and deployment processes

- CICD (Continuous Integrating and Continuous Deployment) approach in building and maturing the Machine Learning models

- Continuously learn from data to reflect the latest customer and market dynamics

- Improving efficiency in models by automating the Data Collection, Data Management, Model Retraining, Model Fine Tuning and Model Governance

- Incorporated best practices in model development, including support for sensitivity analysis, enhanced model monitoring, benchmarking, and analytical reporting

- Researching on new risk models

- Automate the delivery of highly personalized customer services that consider risk levels and smart capital allocation.

- Accelerate risk insights so risk impacts can be assessed when making real-time decisions or for quick decisions

- Make models more accurate by improving algorithms

- Reveal complex relationships hidden in data for better predictions and risk optimization

- Seamless integration across business processes and systems.

- Centralized model inventory with robust version control and change management capabilities