- 28-10-2021

- BPS

- Business Process Solutions

-

Share

Nobody likes disputed bank card charges. Not consumers, and certainly not banks. Card disputes not only cost time and money, but they often cost a customer’s business, too. Yet there’s no getting around it - card disputes and chargebacks have never been more challenging than they are today. According to a recent McKinsey report, card-related payment disputes between consumers and merchants comprise less than 1% of all transactions. Yet the growing complexity of resolving disputes and the evolving nature of how consumers pay for goods and services is creating enormous margin pressure for banks and an increasing potential for lost business.

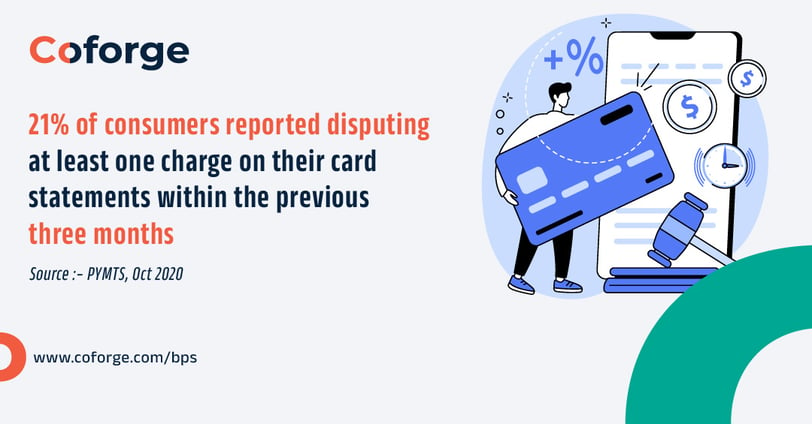

Over the past year and a half, the COVID-19 pandemic has accelerated both the volume of card transactions as well as card disputes, as canceled travel plans, postponed concerts and supply chain disruptions have over-extended dispute resolution processes and led to spikes in operating costs. According to an October 2020 survey of 2,000 consumers by PYMTS and PAAY, 21% of respondents reported disputing at least one charge on their card statements within the previous three months. In addition to these issues, new ways of making digital payments, such as Apple Pay, Venmo and Zelle, continue to take away transaction volumes from banks, eating into their profits. It doesn’t help that resolving card disputes is typically a very complex, disjointed process riddled with inefficiency.

There is constant back-and-forth happening between different call centers, dispute research departments and the back office, and most dispute management work is laden with manual tasks. We know of several banks that have as many as 15 dispute resolution locations, with little orchestration between them. As a result, many banks find themselves over-processing disputes, applying the same process across the board regardless of the dispute amount or merchant history. Frequently, disputes are turned over to third parties for additional research on fraud, which can take up to five days to provide consumers with a response - even though the actual work involved in resolving a case may only take an hour. All of this frequently takes place with ineffective quality assurance to ensure a bank is checking the right regulatory boxes. Surely, there must be a better way. Most banks we speak with realize their biggest obstacle is their fragmented approach to card disputes and their inability to address disputes and chargebacks more holistically.

As a result, a growing number of banks have been rethinking dispute resolution with an eye towards maintaining and even strengthening the customer’s trust. Most banks are discovering that more effective dispute management requires an end-to-end strategy that encompasses four critical issues: faster turnaround times, stronger QC and compliance, lower operational costs and better customer service. Let’s take a look at these in greater detail.

A Need for Speed They call it “the Amazon experience” for a reason: the world’s largest retailer has set a pretty high bar for customer satisfaction. If you’ve ever returned an item purchased on Amazon that wasn’t what you wanted or disputed a charge, the money is back in your account within a few hours. Even the most straight-forward card disputes are rarely resolved this quickly. With an experienced BPO partner, however, banks can access new operating models that leverage agile workflows, guided documentation processes, and automated QC and compliance tools to provide a seamless integration between customer-facing services and back-office operations. The result is an end-to-end dispute resolution strategy that has been proven capable of delivering a 60% faster turnaround time and a 25% improvement in average handling time.

Lower Costs More banks are realizing the key to lowering costs is centralizing customer interactions and leveraging intelligent automation to streamline card disputes. The first part can be accomplished through an omnichannel contact center that supports all dispute intake channels, whether by phone, mail, email or online chat. By centralizing customer interactions through a single dispute and chargeback operations center, for example, banks can achieve significant improvements in first call resolution. The second piece is achieved by leveraging robotic process automation to identify manual processes that can potentially be automated. For instance, by utilizing intelligent and optical character recognition (ICR/OCR) technology, documents can be read and processed in seconds, rather than hours when performed by humans. Automating these processes also reduces the need for manual intervention, which often leads to errors and rework. By accessing intelligent automation, some banks have been able to achieve as much as a 45% reduction in operational costs.

Stronger Compliance Embedding automated RegTech solutions into the dispute resolution process can ensure compliance with state and federal regulations, including Reg Z. Such solutions are currently reducing QC processes that formerly took two hours to less than 30 seconds. Coforge own QC solution, Copasys, for example, enables banks to run every dispute transaction through a checklist that includes not only all applicable regulations, but also a bank’s internal rules. When using a partner capable of combining stringent QC and compliance checks with automation and data analytics, banks are able to achieve compliance testing that is 20 times faster than manual QC - while also ensuring 100% coverage and 100% accuracy of existing regulations and business rules. Even better, they gain higher levels of business intelligence and reporting, which can be used to continually improve dispute management.

Happier Customers Psychologists call it “the recency effect,” which essentially means we tend to remember the last interaction we had with someone. If the last experience your customer had was “I had a bad charge on my card and it did not go well,” they are less likely to use that card again. On the other hand, if the dispute was resolved quickly and the customer had their money back in a few hours, the experience they remember will be a positive one. Happier customers can be created even in the most difficult of circumstances.

For example, one our clients, a top 20 U.S. bank, was experiencing a huge spike in card disputes triggered by the COVID-19 pandemic. Coforge Card Dispute Center of Excellence Team not only helped manage the spike in disputes but also achieved faster dispute resolutions, which improved customer satisfaction levels. We also saved the bank money. Previously, the banks’ write-off threshold had grown from $20 to $50 per disputed transaction, creating significant losses. We reviewed all disputed transactions to identify whether chargeback rights were available. As a result, we were able to recover $574,000 in losses from earlier write-off cases. The bottom line is that card disputes and chargebacks are not something that can be solved overnight. However, banks that are serious about reducing losses and improving customer satisfaction owe it to themselves to rethink their approach to card disputes and find a partner that can provide maximum efficiency with minimal effort. By doing so, they’ll not only be able to manage card disputes more cost-effectively. They’ll also create more loyal customers, who know that if there's a problem, their bank is going to fix it.